When budgeting for a family of five, distributing your income into various categories based on percentages can be helpful. A percentage-based budget is a guideline and will not always be 100% accurate. Still, you can adjust your budget categories in the budget percentage range depending on your family’s needs and your family’s financial situation. Even though these percentages are a guideline, they are a great tool that you can start with to start the budgeting journey for a family of five.

Also, check out these great budgeting tools on Amazon:

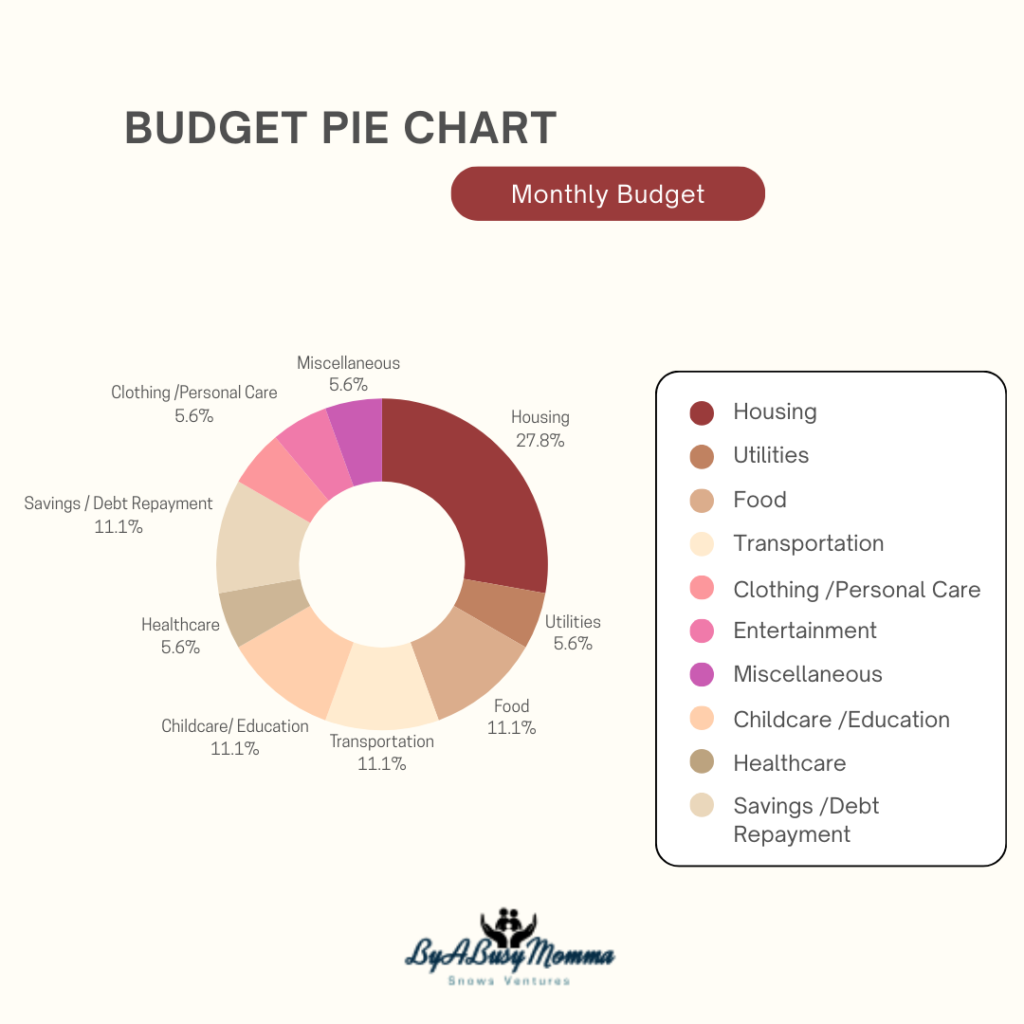

While these percentages can vary depending on individual circumstances, here is a general breakdown that can serve as a starting point:

- Housing: 25-35% of your monthly income. This includes rent or mortgage payments, property taxes, and home insurance.

- Utilities: 5-10% of your monthly income. This category covers expenses like electricity, water, gas, internet, and phone bills.

- Food: 10-15% of your monthly income. This includes groceries and dining out expenses.

- Transportation: 10-15% of your monthly income. This category covers costs related to transportation, such as car payments, fuel, insurance, maintenance, and public transportation expenses.

- Childcare and Education: 10-20% of your monthly income. This includes expenses for childcare, school fees, extracurricular activities, and educational materials.

- Healthcare: 5-10% of your monthly income. This category covers health insurance premiums, copayments, prescription medications, and routine medical expenses.

- Savings and Debt Repayment: 10-20% of your monthly income. Allocate a portion of your income to savings and debt repayment, including building an emergency fund and paying off any debts.

- Clothing and personal care: 5-10% of your monthly income. This category includes expenses for clothing, footwear, and personal care items for each family member.

- Entertainment and recreation: 5-10% of your monthly income. Set aside funds for family outings, vacations, hobbies, and entertainment expenses.

- Miscellaneous expenses: 5-10% of your monthly income. This category covers unexpected or miscellaneous expenses that may arise, such as home repairs, car maintenance, gifts, or unforeseen medical expenses.

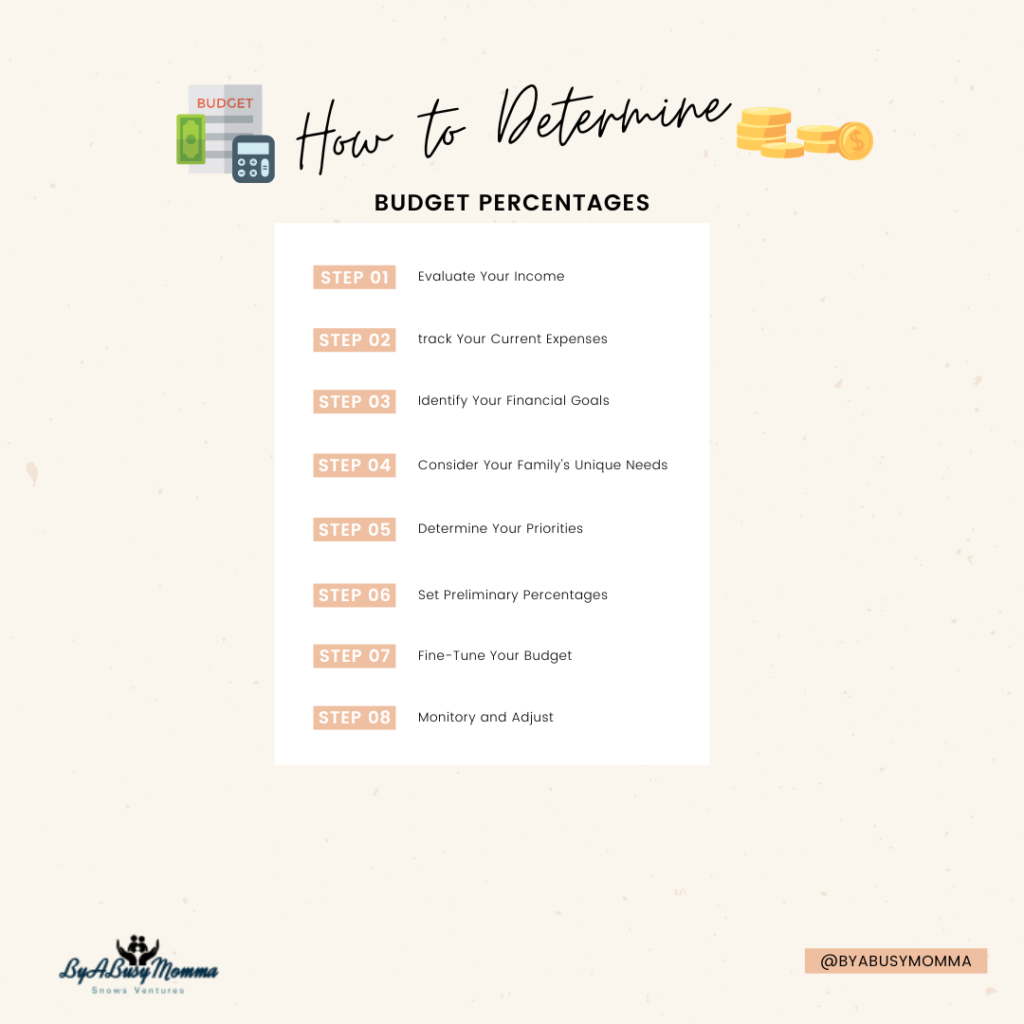

Determining the appropriate percentages for each budget category based on your circumstances involves considering several factors.

Here’s a step-by-step approach to help you determine these percentages:

Evaluate your income: Start by assessing your total monthly income. Calculate your net income, the amount you take home after taxes and other deductions. This will be the basis for allocating percentages to different categories.

Track your current expenses: Review your spending over the past few months to understand where your money is going. Categorize your expenses into different categories, such as housing, utilities, food, transportation, etc. This will give you an idea of your current spending patterns.

Identify your financial goals: Determine your short-term and long-term financial goals. For example, you might have goals such as saving for a down payment on a house, paying off debt, funding education, or building an emergency fund. Prioritize these goals to guide your budgeting decisions.

Consider your family’s unique needs: Think about the specific needs of your family of five. Consider factors such as the ages of your children, any special diet or healthcare requirements, educational expenses, and any other unique circumstances that may impact your budget.

Determine your priorities: Based on your income, goals, and family needs, identify your financial priorities. Some categories may require more of your budget than others, depending on what is most important to you. For example, if retirement savings are a top priority, you may allocate a higher percentage to retirement savings.

Set preliminary percentages: Assign preliminary percentages to each budget category based on your priorities using the information gathered. Try to allocate percentages you feel comfortable with that align with your financial goals.

Fine-tune your budget:

- After a detailed budget that reflects these allocations after setting preliminary percentages.

- allocate your income to each category, ensuring that your total allocations add up to 100%.

- Adjust the percentages to make the budget work for you.

Monitor and adjust: Once you implement your budget, regularly track your expenses and compare them to your budgeted amounts. This will help you identify areas where you need to adjust your percentages. Over time, specific categories need more or less of your budget, and you can make changes accordingly.

A reasonable budget for a family of five depends on various factors, including location, lifestyle, income level, and financial goals. Remember, these are general guidelines, and your budget should be tailored to your unique financial goals. It’s essential to track your expenses, review your budget regularly, and make adjustments to ensure that your spending aligns with your priorities and financial capabilities.

Here are some additional considerations and categories to include when creating a budget for a family of five:

Insurance: In addition to health insurance, you may need to consider other types of insurance, such as life insurance, disability insurance, and homeowner’s or renter’s insurance. These costs can vary depending on your coverage needs and insurance provider.

Child-related expenses: Depending on your children’s ages, you may have additional costs such as diapers, formula, baby food, clothing, school supplies, and extracurricular activities. Be sure to allocate a portion of your budget to cover these costs.

Clothing and personal care: Budget for clothing and footwear for each family member, as well as personal care items like toiletries, haircuts, and grooming products. The amount you allocate will depend on your family’s preferences and needs.

Entertainment and recreation: Set aside funds for family outings, vacations, hobbies, and entertainment expenses. This could include activities like movies, visiting amusement parks, or participating in sports or recreational clubs.

Miscellaneous expenses: It’s a good idea to have a category for miscellaneous or unexpected expenses that may arise, such as home repairs, car maintenance, gifts, or unexpected medical expenses. Allocating a small percentage of your budget to this category can provide a buffer for unforeseen costs.

Taxes: Consider the impact of taxes on your budget. Depending on your income level and tax obligations, you may need to allocate a portion of your budget for income taxes, property taxes, or other tax liabilities. When creating your budget, it’s essential to factor in taxes. This includes income, property, and other applicable taxes based on location and circumstances. Consider consulting a tax professional to ensure you accurately estimate your tax obligations.

Financial goals: If you have specific goals, such as saving for a down payment on a home, funding education, or retirement savings, allocate funds towards those goals in your budget. Create separate categories for each goal and determine how much you can contribute monthly.

Emergency Fund: Building an emergency fund is crucial for financial stability. Aim to set aside a portion of your monthly income into an emergency savings account. Ideally, it would help if you aimed to have three to six months’ living expenses in your emergency fund to cover unexpected expenses or income disruptions.

Debt Repayment:

- If you have outstanding debts such as credit card debt, student loans, or a mortgage, allocate a portion of your budget towards debt repayment.

- Focus on paying off high-interest debts first while making minimum payments on other debts.

- Consider using the debt snowball or avalanche method to accelerate your debt repayment.

Retirement Savings: It’s never too early to start saving for retirement. Allocate a portion of your budget towards retirement savings, such as contributing to employer-sponsored retirement plans like 401(k) or individual retirement accounts (IRAs). The earlier you start saving, the more time your investments have to grow.

Education Savings: If you have children and want to save for their education expenses, consider setting up a dedicated education savings account, such as a 529 plan. Allocate funds each month towards this account to help cover future education costs.

Communication and Family Involvement: Involving the entire family in budgeting can foster financial responsibility and teamwork. Discuss financial goals and priorities with your spouse and children and encourage open communication about money matters. This can help create a shared understanding and commitment to the budget.

Seek Professional Help if Needed: If you find it challenging to create or stick to a budget, consider seeking help from a financial advisor or a certified financial planner. They can guide your circumstances and help you make informed financial decisions.

It is essential to regularly review and adjust your budget based on income, expenses, and changes in financial goals. Remember, budgeting is all about finding a balance between your income, expenses, and financial goals. Regularly reviewing and adjusting your budget, staying disciplined, and tracking your progress will help you achieve economic stability and work toward your family’s financial aspirations.